HRP Technical Reference: Evidence Standards, Edge Cases & Record-Linking (1978–2010)

Scope, audience and approach

This reference is written for practitioners (CAB, charities, welfare rights, journalists). It focuses on evidence sufficiency, dated corroboration per tax year, identity/address bridging and an auditable workflow that reduces rework.

1) Policy background and data-linking context

HRP (6 April 1978–5 April 2010) shielded parents/carers from NI gaps. Under-recording arose due to: (a) pre-May 2000 Child Benefit forms often lacking NI numbers; (b) name/address changes without a bridging audit trail; and (c) legacy paper systems that were never fully reconciled.

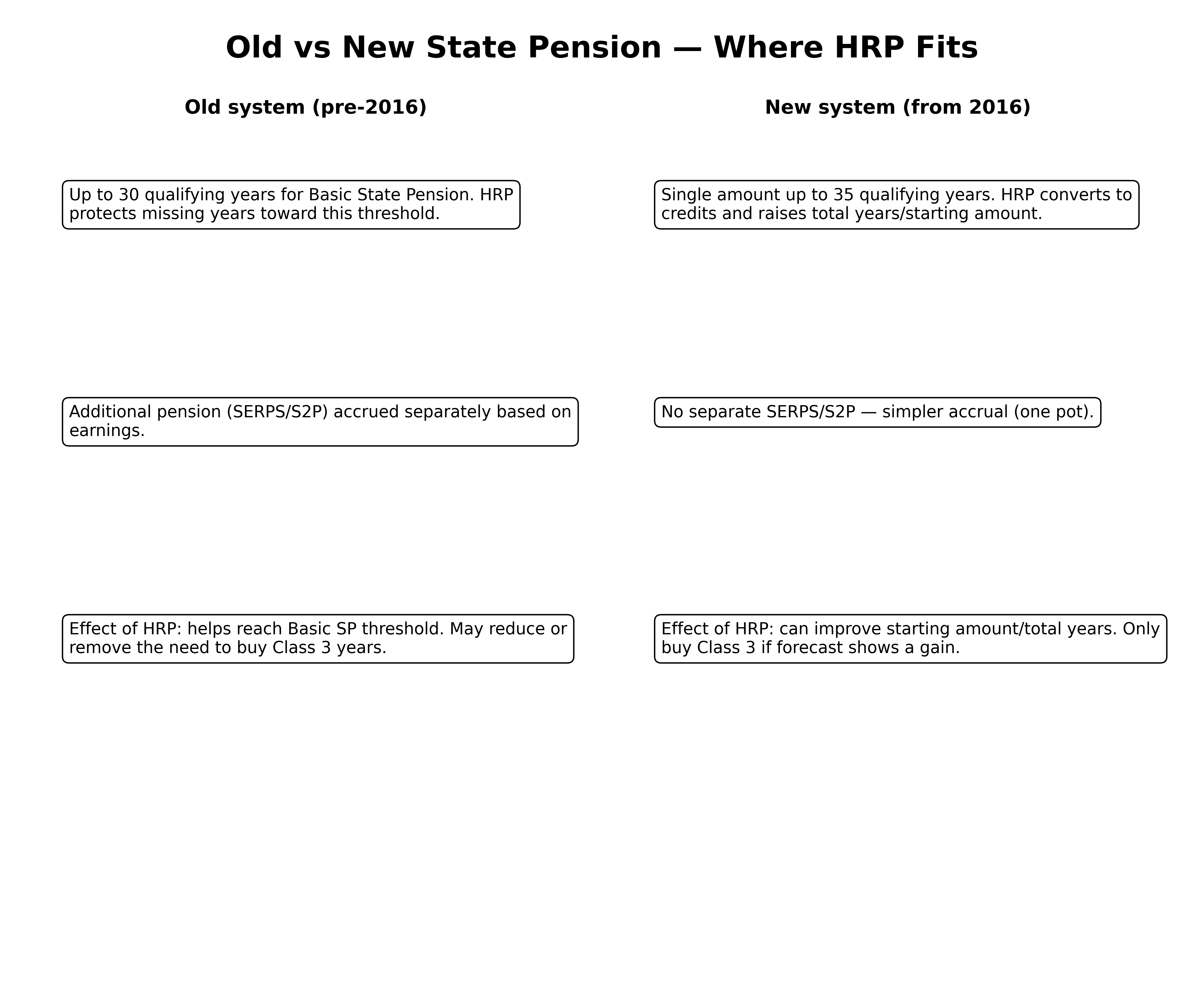

From April 2010, HRP ended and NI credits began. HRP corrections can affect both pre-2016 and post-2016 pension regimes via starting amounts and total qualifying years.

2) Eligibility pathways (formal definitions)

• CB-holder route — claimant received Child Benefit for a child in the household; relevant tax years may qualify for HRP.

• Main-carer transfer — Child Benefit was in a partner’s name; claimant was the day-to-day carer; independent evidence must substantiate primary care.

• Pre-2002 caring route — ~35 hours/week care for a person on a qualifying benefit; needs health/LA letters naming claimant plus benefit proof.

• Special households — adoption, fostering, kinship guardianship; rely on LA orders/letters plus education/health corroboration naming claimant.

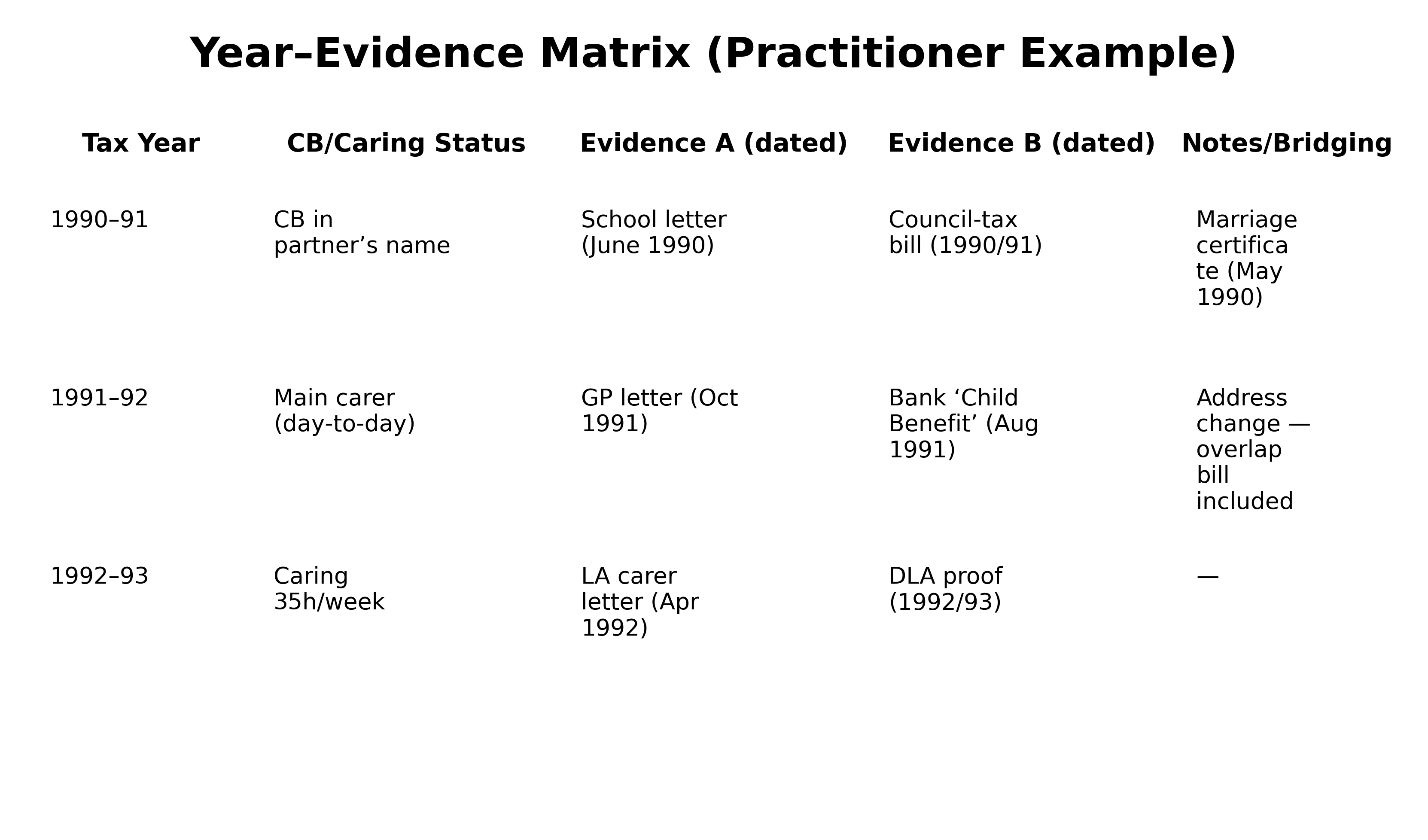

3) Evidence hierarchy and sufficiency (map to tax years)

• Primary — Child Benefit award letters; LA/GP/hospital letters naming claimant with dates; adoption/placement orders.

• Secondary — bank entries showing ‘Child Benefit’; school letters naming claimant + child; council-tax/tenancy showing household composition.

• Bridging — marriage certificate/deed poll + overlapping official bills connecting old→new names/addresses (ensure a document spans the change month).

• Insufficient alone — undated letters; personal statements; generic references not tied to tax years or address history.

Caption: “Figure A — Year–evidence matrix (practitioner example rows).”

4) Record-building workflow (repeatable, auditable)

1) Intake & permissions — capture historic names/addresses, Child Benefit facts (who claimed; dates; children), caring periods, and consent to contact third parties.

2) Matrix build — grid all candidate tax years: status → document A (dated) → document B (dated) → notes/bridging.

3) Retrieval — instruct schools/GPs/LAs/banks to issue letters that name the claimant and include precise dates within the tax year(s).

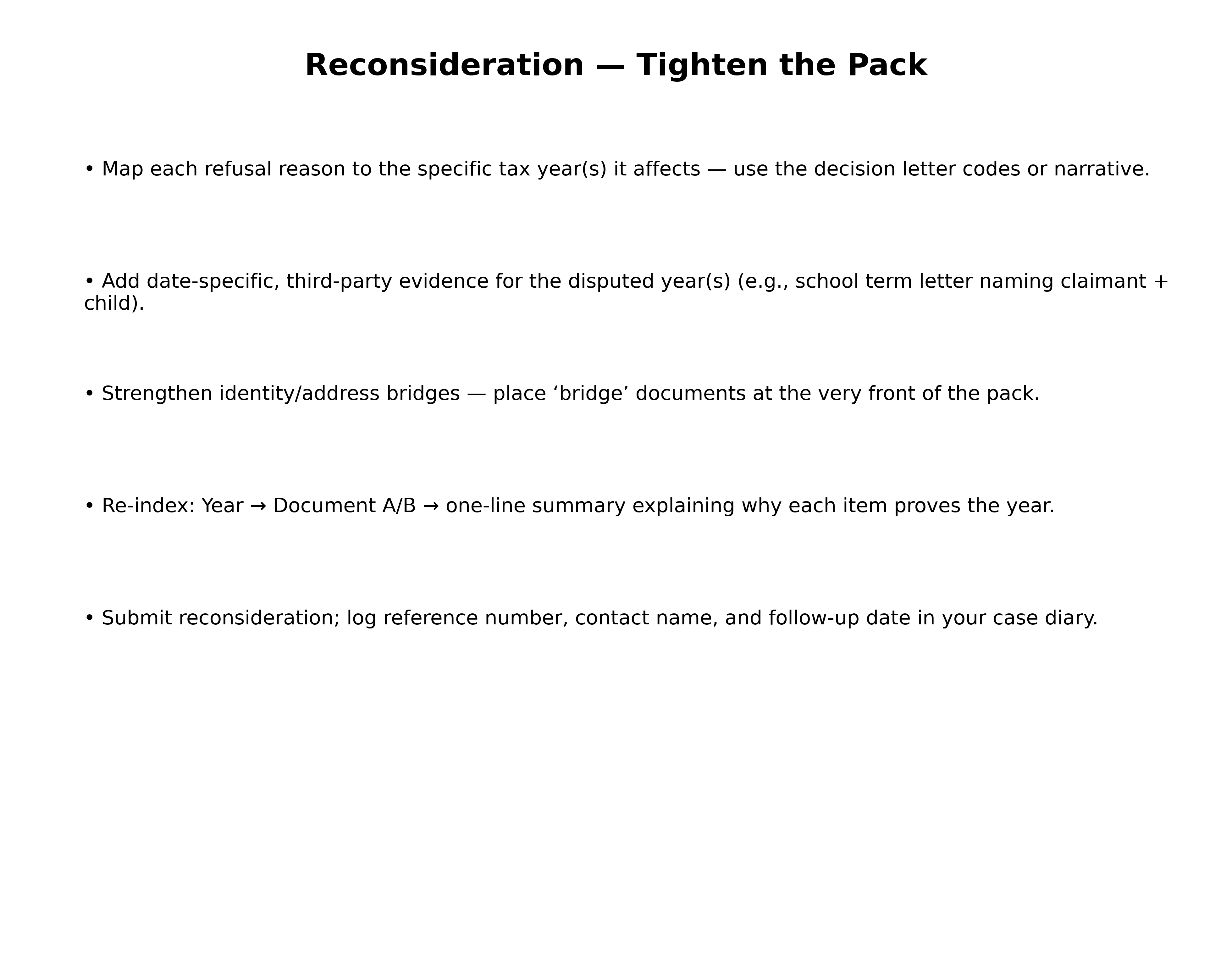

4) Pack assembly — paginate exhibits; place identity bridge before the first year affected by a change; index exhibits.

5) Submission — online CF411 where possible; tracked post if not; retain copies; log reference numbers.

6) Post-decision — reconcile NI record; re-run forecast; weigh Class 3 only if forecast shows a monetary gain for the client.

Caption: “Figure B — Reconsideration checklist: map refusal → add dated evidence → re-index → resubmit.”

5) Submission protocol and correspondence discipline

Use a succinct covering schedule: each claimed tax year and the two exhibits relied upon. Maintain a contact log (date/time/agent/summary). If identity is queried, resend the bridge pack at the top.

For partial refusals, map refusal codes to years, add stronger dated evidence, and submit a reconsideration.

6) Edge cases and worked examples

• Alternating care / separated parents — prefer school term letters naming the responsible adult; combine with council-tax for household facts.

• Multiple name changes — chain legal documents; ensure at least one monthly bill overlaps the change month.

• Cross-border moves — include immigration/visa or overseas school/GP records; add translations where applicable.

• Deceased estates — executor applies, encloses death certificate, and compiles the same year-evidence matrix.

Worked example — Main-carer transfer, 1991–93: Child Benefit in partner’s name; claimant named as primary carer in two school letters per tax year; household evidenced by joint council-tax. Outcome: HRP credited for both years.

Caption: “Figure C — Old vs new State Pension: HRP interaction and when Class 3 may still be value-adding.”