Many people only start checking Home Responsibilities Protection (HRP) after they have already moved abroad, retired overseas, or returned to the UK after years away. That creates an understandable worry: does living abroad now stop you correcting a historic UK National Insurance record issue?

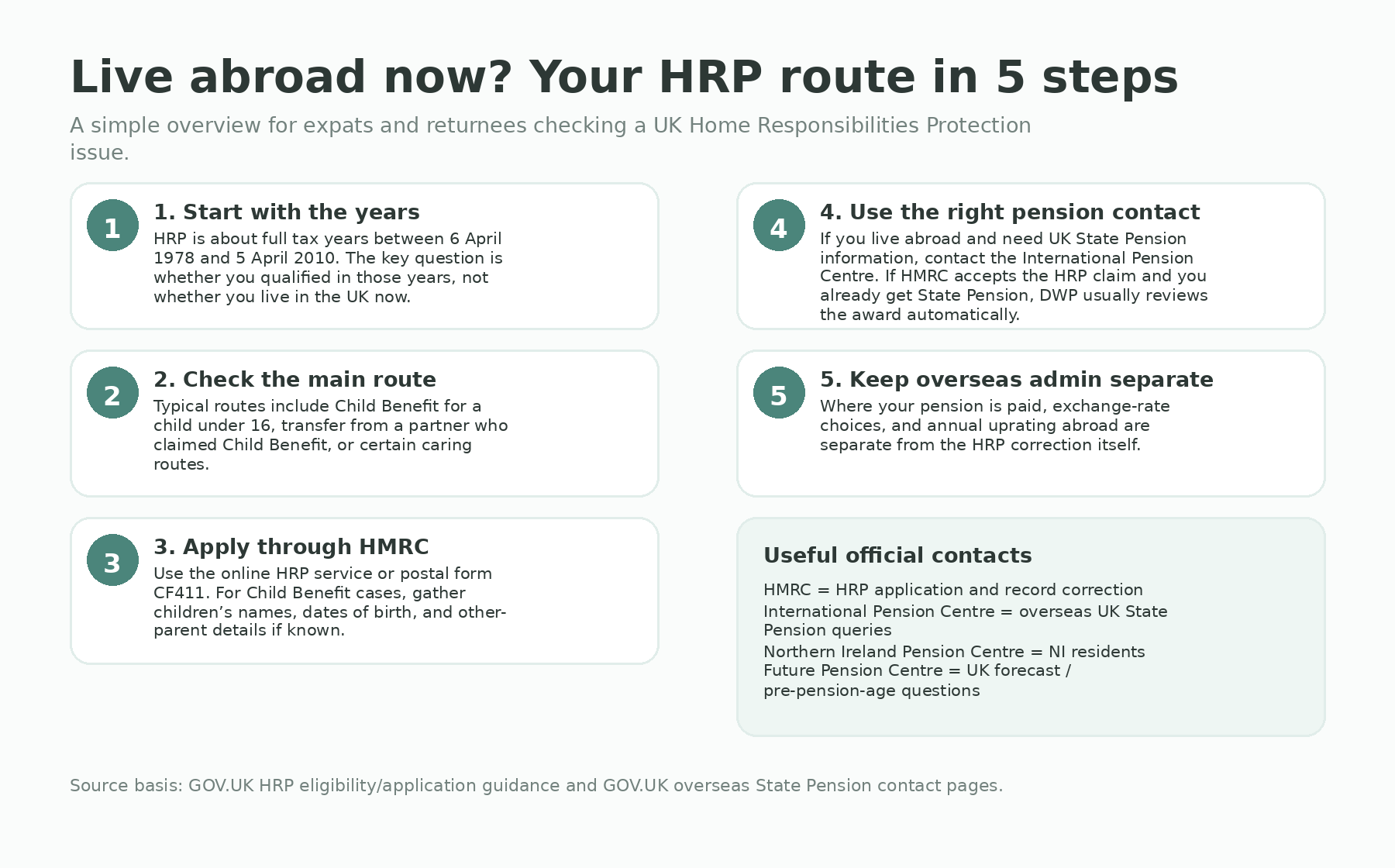

Short answer: not usually. The current GOV.UK guidance focuses on whether you qualified for HRP in the relevant full tax years between 6 April 1978 and 5 April 2010, and HMRC runs the application route. Your present address matters for contact and payment administration, but it is not the core HRP test.

What matters first is the historic UK record. GOV.UK says HRP can apply for full tax years between 1978 and 2010 if, for example, you were awarded Child Benefit for a child under 16, were the main carer while a partner claimed Child Benefit, or qualified through certain caring routes. That means an expat, a returnee, or someone planning to leave the UK can still have a genuine HRP issue to correct if the underlying years fit the rules.

1) What living abroad does — and does not — change

Living abroad now mainly changes the administration around your State Pension, not the historic facts HMRC looks at when deciding HRP. In practice, overseas readers usually need to separate two different questions:

• Did I qualify for HRP in the years I was caring?

• Who should I contact now that I live outside the UK?

That split matters. If you mix the two together, it becomes easy to assume that an overseas address makes the claim impossible. The official guidance does not frame it that way. The HMRC pages ask whether the qualifying conditions existed in the relevant years and then explain the application route.

2) The main HRP routes expats and returnees should check

The most common route is historic Child Benefit. GOV.UK says you can apply for HRP if, for a full tax year between 1978 and 2010, you were awarded Child Benefit for a child under 16. The same page also recognises partner-transfer situations, where one partner claimed Child Benefit but the other was the main carer.

There are also caring routes. GOV.UK says HRP may apply where you were getting Income Support because you were caring for someone who was sick or disabled, or where you were caring for a sick or disabled person who was claiming certain benefits. Foster carers and certain kinship carers also have a route for later years in the HRP period.

For overseas readers, one practical point is worth stressing: moving country later on does not change what happened in those earlier tax years. If the UK record is incomplete, it is still worth checking.

3) Who should you contact if you live abroad?

This is the part that confuses most people.

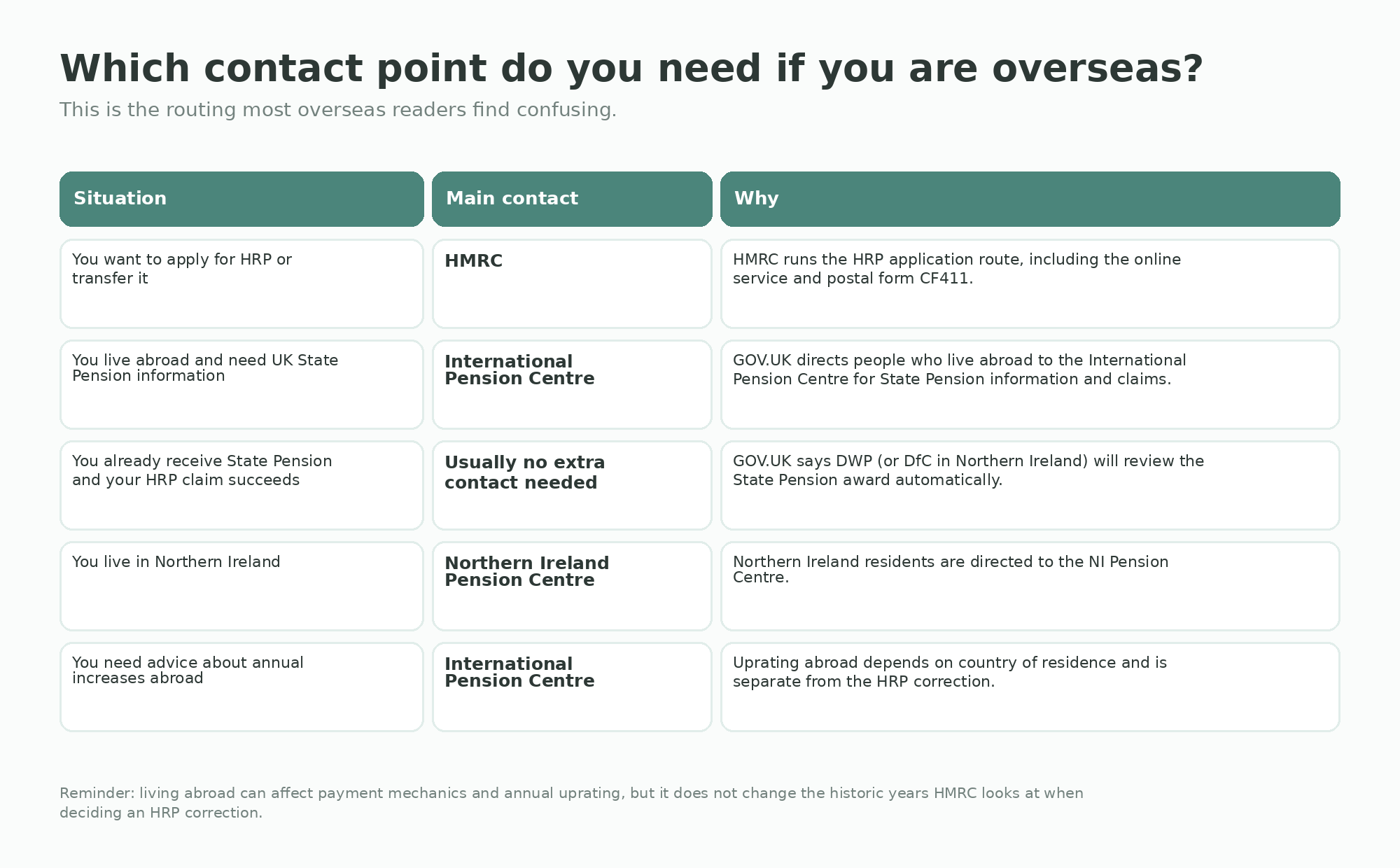

For the HRP application itself, the official route sits with HMRC. GOV.UK says you can use the online service or postal form CF411 to apply for Home Responsibilities Protection or to transfer it from a spouse or partner. For Child Benefit cases, HMRC says you should include the names and dates of birth of all children, plus details of the other parent if known.

For UK State Pension questions when you live abroad, GOV.UK directs people to the International Pension Centre. That is the contact point for advice or information about pensions and benefits if you live abroad or have lived abroad. If you are in Northern Ireland, GOV.UK points residents to the Northern Ireland Pension Centre instead.

If you are already receiving State Pension and your HRP claim succeeds, GOV.UK says the Department for Work and Pensions, or the Department for Communities in Northern Ireland, will review your State Pension award. In other words, you do not normally need to start a separate chase just because the HRP correction has been accepted.

4) What changes if you already get your UK State Pension overseas?

Once you are already drawing a UK State Pension abroad, three separate things can be in play at the same time:

• the historic HRP correction on your National Insurance record

• the recalculation of the pension itself

• the overseas payment rules for where and how you are paid

GOV.UK says you can claim State Pension abroad if you have paid enough UK National Insurance contributions to qualify, and it provides specific overseas claim forms and payment forms through the International Pension Centre. It also says that if you live part of the year abroad, you must choose which country you want the pension paid in; you cannot split the payment country across the year.

That is useful because many readers assume HRP, payment destination, and exchange-rate choices are one and the same issue. They are not. A successful HRP correction may improve the pension position, but the payment mechanics still follow the overseas pension rules.

GOV.UK also says that if you choose to be paid into an overseas account, you will normally need the international bank account number (IBAN) and business identifier code (BIC). If you choose payment in local currency, there is currently a conversion charge before payment. If you choose pound sterling, there is no conversion charge.

5) A separate issue: annual increases abroad

This is not strictly an HRP rule, but it matters to overseas readers. GOV.UK says UK State Pension only increases each year in certain places, including the EEA, Gibraltar, Switzerland, and certain countries with a social security agreement with the UK. If you live outside those countries, yearly increases generally do not apply while you stay there.

That does not mean HRP is pointless. It simply means you should keep two ideas separate: first, whether the underlying UK pension has been corrected; second, how annual uprating works in the country where you live.

6) What evidence helps when you are abroad or have lived abroad?

The core evidence depends on your route, not your postcode. For Child Benefit cases, HMRC says you will need children’s names and dates of birth, and other-parent details if known. GOV.UK also says you can include supporting evidence such as a Child Benefit award letter or a bank statement showing Child Benefit payments.

For expats and returnees, the useful practical addition is organisation. Put together a simple pack with:

• a short timeline of your names and addresses

• the tax years you think may be affected

• children’s names and dates of birth

• any Child Benefit letters, payment evidence, or related paperwork you still have

• a copy of your National Insurance record and State Pension forecast, if available

That sort of pack is not a special overseas legal requirement. It is simply the clearest way to reduce confusion where a case spans old UK records and a current overseas address.

7) A simple order to follow

1. Check the official HRP eligibility guidance first.

2. Get your National Insurance record and State Pension forecast if you can.

3. Identify the years that look wrong and the route that may apply.

4. Apply to HMRC through the official online service or CF411 postal route.

5. Use the International Pension Centre for overseas State Pension questions, not for the initial HRP application.

Frequently asked questions

Can I still claim HRP if I moved abroad years ago?

Possibly, yes. The key issue is whether you qualified in the relevant full tax years, not the fact you live abroad today.

Do I need to move back to the UK to sort it out?

The current HMRC guidance does not present current UK residence as the core test for HRP. The practical issue is usually making sure you use the right official contact route.

If I already receive UK State Pension overseas, do I need to contact DWP separately after HMRC accepts HRP?

Usually not. GOV.UK says DWP, or the Department for Communities in Northern Ireland, will review the State Pension award if the HRP claim succeeds.

Will a successful HRP claim reduce my pension?

No. GOV.UK says that if a claim for missing HRP is successful, State Pension will increase or stay the same — it will not decrease.

What if I only live abroad for part of the year?

GOV.UK says you must choose which country you want your pension to be paid in. You cannot be paid in one country for part of the year and another for the rest of the year.

Check eligibility in 60 seconds

Helpful internal Evanshaw links

• How Long Do HRP Claims Take? Timeline, Tracking, and What to Do If You Hear Nothing

• CF411 vs CF411A: which form do I need?

Official GOV.UK links used in this draft

• Apply for Home Responsibilities Protection

• Home Responsibilities Protection: eligibility

• Quick guide to HRP communication resources

• International Pension Centre

• Claim State Pension if you live abroad