If HMRC has accepted an HRP correction but your State Pension has not visibly gone up, it is easy to think something has gone wrong. Families often assume that a successful Home Responsibilities Protection decision must always produce a higher weekly figure or a lump sum of arrears.

Official GOV.UK guidance is more careful than that. The current wording says that if your claim for missing HRP is successful, your State Pension will increase, or stay the same — it will not decrease. That small phrase, “or stay the same”, is one of the most important lines in the whole HRP process.

In practice, a successful HRP decision can leave you in one of several different positions. Your pension may go up. It may stay exactly where it is because you were already at the maximum available under your rules. Or your State Pension may increase but your overall household income may feel broadly unchanged because Pension Credit or another means-tested top-up adjusts around it.

The short version

A successful HRP claim does not guarantee a bigger weekly payment. GOV.UK expressly says a successful claim can make State Pension increase or stay the same.

• if you reached State Pension age before 6 April 2010, HRP often worked by reducing the number of qualifying years needed for a full basic State Pension, so it may not change your amount if you were already at the full rate;

• if you reached State Pension age on or after 6 April 2010, HRP was converted into National Insurance credits only if you needed them, so an award may correct the record without lifting your weekly amount;

• if you are on the new State Pension, contracted-out history can still limit what extra years do for your visible weekly figure;

• if your State Pension does rise, Pension Credit or another means-tested top-up may reduce, so your total income can look similar even though the pension itself changed;

• if HMRC has corrected the record but DWP has not yet completed the review, an apparent “no increase” may simply be a timing issue rather than the final answer.

First question: has your pension really stayed the same, or has the record changed first?

This is the best place to start. A lot of people compare one payment amount to the next and assume the case has finished. But HRP cases usually move in stages. HMRC corrects the National Insurance record. Then, if you are already receiving State Pension, DWP or the Department for Communities in Northern Ireland reviews the pension award.

That is why the first practical check is not just your bank payment. Check whether the National Insurance record has been corrected, whether you have had a revised State Pension notice, and whether the effective date on any review letter has already passed. A corrected record and a revised payment do not always arrive on exactly the same day.

So before assuming the claim has “failed”, separate these questions: has the HRP decision been accepted; has the NI record been updated; has the State Pension award been reviewed; and has any knock-on effect on benefits already been processed?

What GOV.UK actually says about successful HRP claims

The most important official wording is in the current HRP communications material. GOV.UK says that if your claim for missing HRP is successful, your State Pension will increase, or stay the same — it will not decrease. It also says that if you are receiving State Pension, DWP will review your award and you do not need to contact them separately.

That wording matters because it corrects a very common misunderstanding. HRP is there to protect the State Pension position that should have existed. It does not promise a new bonus on top of an already-maxed-out entitlement. In other words, the award can be successful even if the outcome is to confirm that your correct pension is the same as the one already in payment.

The official guidance also warns that if your State Pension increases, the change can affect Income Tax and benefits you are entitled to, including Pension Credit. So sometimes people do get a higher State Pension but feel that their overall finances have barely moved because a top-up has reduced.

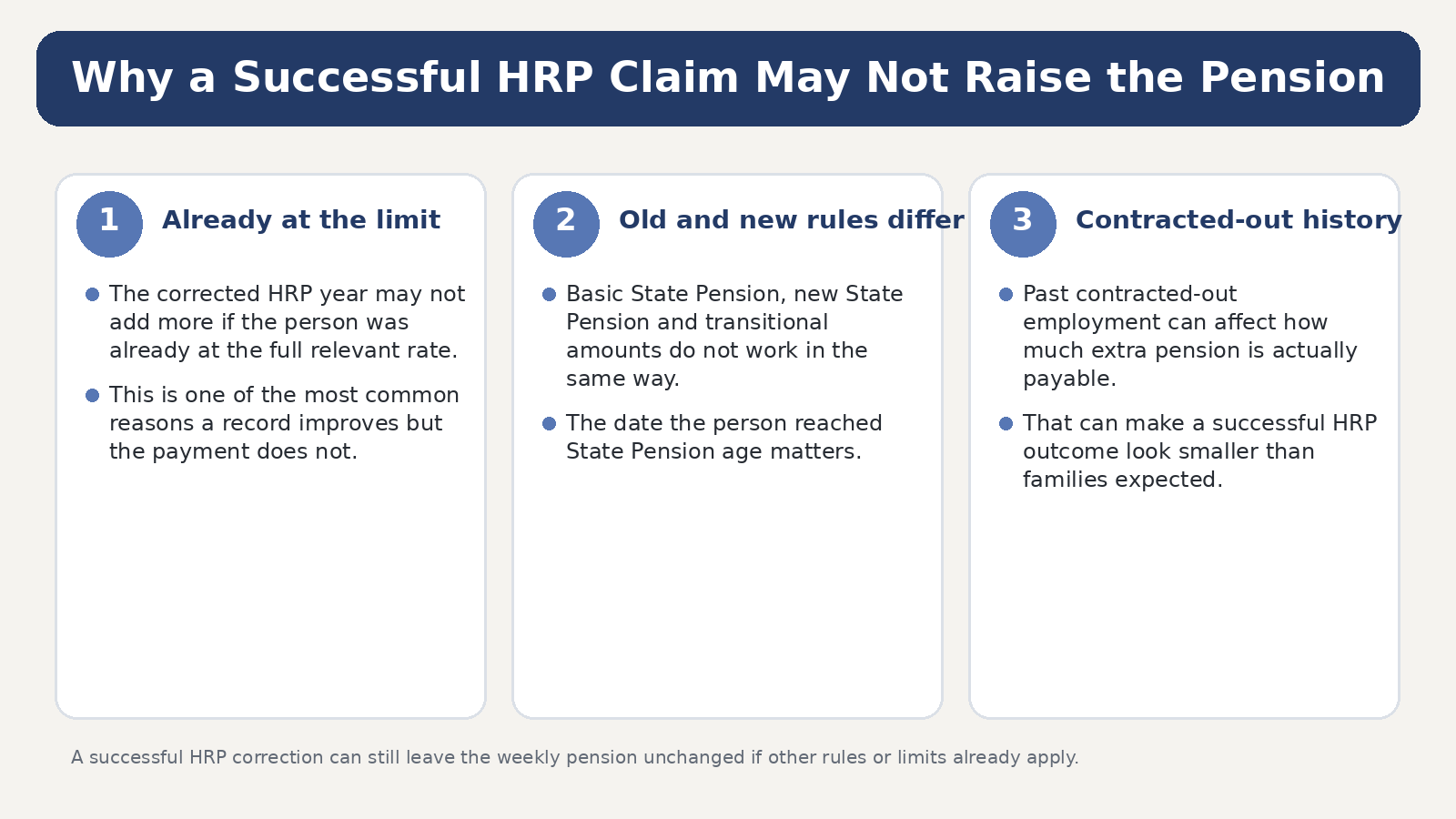

Reason 1: you were already at the maximum available under your rules

This is one of the most common reasons for confusion. For many people who reached State Pension age before 6 April 2010, HRP did not behave like an extra paid year added on top of everything else. Instead, it reduced the number of qualifying years needed to get the full basic State Pension.

That means a successful correction can still leave the weekly amount unchanged if the person was already at the full basic rate once their wider history was taken into account. The HRP decision still matters because it puts the record right, but the visible pension figure may not move.

A similar principle can apply after 6 April 2010. GOV.UK says HRP was converted into National Insurance credits, if you needed them, up to a maximum of 22 qualifying years. The phrase “if you needed them” is important. If the record correction does not create extra usable entitlement under the rules that apply to you, the weekly pension may stay where it is.

Reason 2: old/basic State Pension rules and new State Pension rules are not the same

Families often compare different cases and assume one person’s outcome should match another’s. That is risky with HRP. Someone under the old/basic State Pension framework may see a different effect from someone under the post-2016 new State Pension framework, even if both had missing HRP for similar child-caring years.

Under the new State Pension, your amount depends on your National Insurance record and your transitional starting amount. GOV.UK also says that if you were contracted out before 6 April 2016, an amount is taken off your new State Pension because you and your employer paid less into the State system and more into a workplace or private pension.

That is why a person can have a successful HRP correction and still not see the simple “one missing year equals one obvious uplift” result they expected. The old system, the 2010 conversion, the 2016 transition, and any contracted-out history all have to be read together.

• before 6 April 2010, HRP could reduce the number of qualifying years needed for a full basic State Pension;

• from 6 April 2010, HRP could convert into credits if needed;

• from 6 April 2016, the new State Pension introduced a different framework and transitional starting amount;

• contracted-out history can mean that even with more qualifying years, the visible pension figure does not change in the simple way people expect.

Reason 3: your State Pension rose, but another benefit moved the other way

This is a different kind of “stayed the same” result. Sometimes the State Pension itself has increased, but the person also receives Pension Credit. Because Pension Credit tops income up to a minimum level, an increase in State Pension can mean Pension Credit reduces.

So the person is not imagining things if the household position feels flat. The pension may genuinely have risen while the top-up fell. In that situation, the correct conclusion is not that HRP “did nothing”. It is that the source of the income changed: more from State Pension, less from means-tested support.

This is also why post-award checking matters. If you receive Pension Credit, Housing Benefit or Council Tax Reduction, you need to understand how a revised pension figure may ripple through the rest of the file.

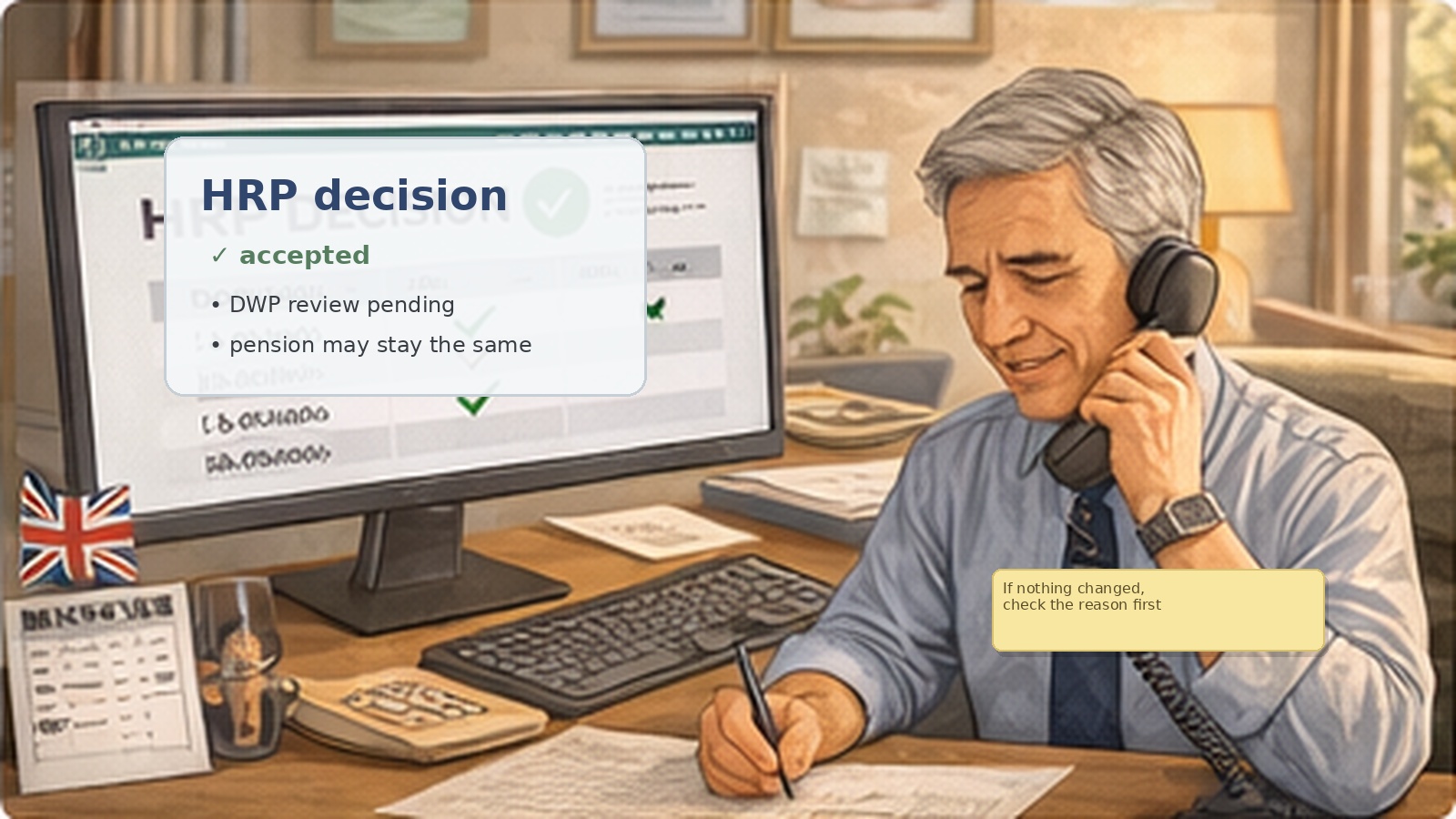

Reason 4: you may be looking too early

Some people receive the HRP success letter and immediately expect the next pension payment to change. But the official guidance says DWP reviews the award after the HRP correction. In real life, that means there can be an interval between the record being fixed and the pension review being fully reflected in notices or payment lines.

So if you have a successful HRP outcome and nothing seems different yet, do not jump straight to the conclusion that there will never be an increase. First check the date of the HRP decision, whether you are already over State Pension age, whether a revised award letter has been issued, and whether any arrears explanation has followed.

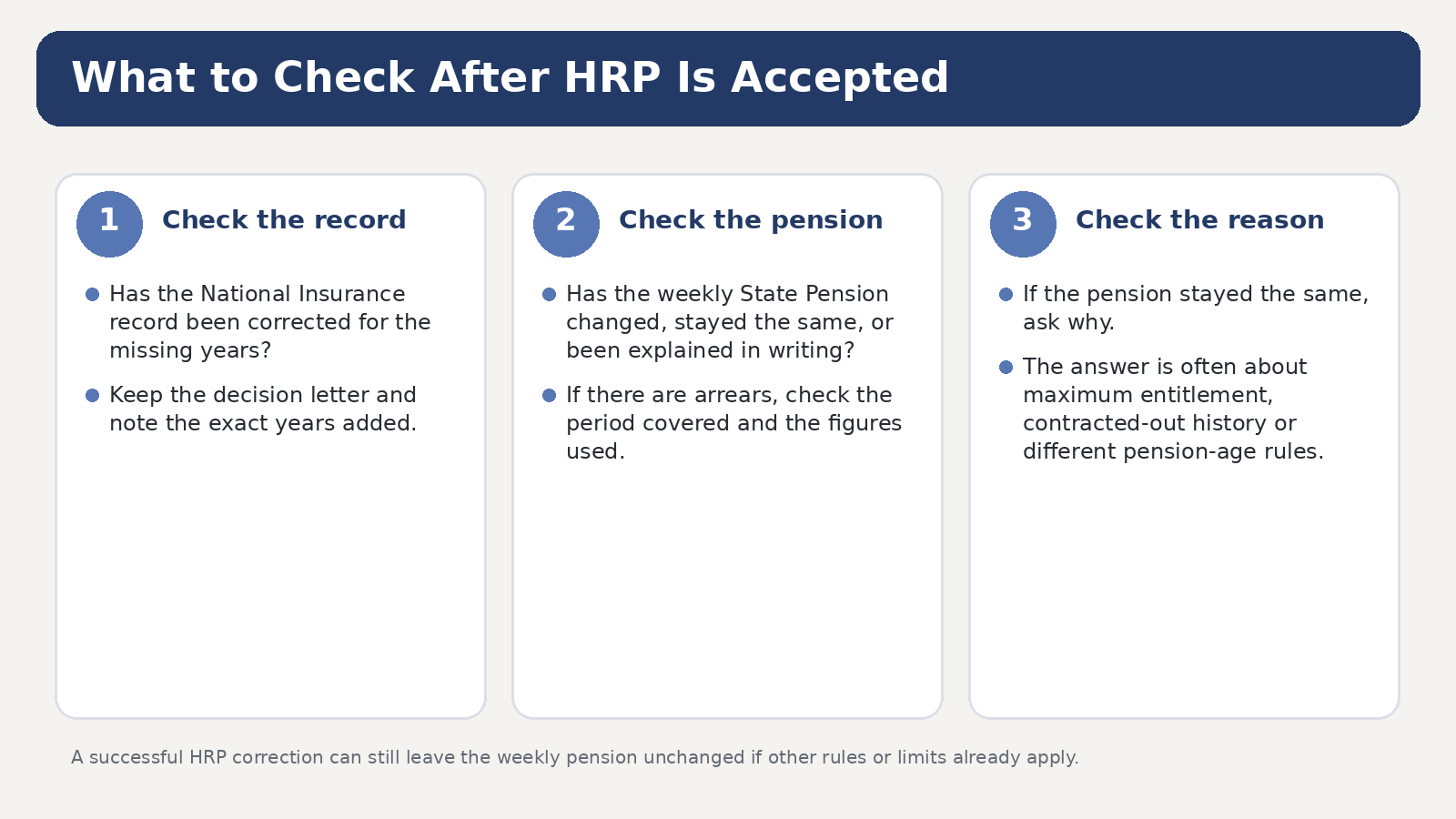

What should you gather and compare after a successful HRP decision?

Keep the post-decision review simple and document-led. In most cases you should line up the papers in this order:

• the HRP acceptance or correction letter;

• your latest National Insurance record or screenshot showing the corrected position if available;

• your old State Pension award letter or forecast;

• any revised State Pension notice showing the new weekly amount or confirming it is unchanged;

• any Pension Credit or related benefit notice issued after the pension review;

• notes of dates, phone calls and who told you what.

This matters because many apparent problems are really comparison errors. People compare the wrong weeks, the wrong letters, or a bank payment before the recalculation has fully landed. A tidy timeline often resolves the confusion very quickly.

Common mistakes when a successful HRP claim seems to change nothing

The most common avoidable mistakes are:

• assuming that a successful HRP decision must always create extra weekly State Pension;

• forgetting that old/basic State Pension rules, the 2010 conversion and the new State Pension rules are different systems;

• ignoring contracted-out history when judging a new State Pension result;

• looking only at the pension payment and not at Pension Credit or other linked benefits;

• checking too early, before the DWP review has fully completed;

• treating a corrected record as “useless” just because the first visible payment does not look higher.

Check eligibility in 60 seconds

Final takeaway

A successful HRP claim can absolutely leave the visible pension figure unchanged. GOV.UK says so in terms. That does not mean the correction was pointless or wrong. It usually means one of four things: the person was already at the maximum available entitlement under their rules, the case sits inside a different pension framework than the family expected, another benefit has adjusted around the pension increase, or the review is still working through the system.

So the safest approach is not to ask only, “Did the bank payment go up?” Ask the fuller question: was the record corrected, which State Pension rules apply, did a revised award issue, and did any linked benefits move at the same time?

Helpful internal Evanshaw blog links

• HRP & Pension Credit — What Changes When Your State Pension Goes Up?

• DWP State Pension Forecast — How to Read It for HRP

• HRP Under Old vs New State Pension Rules — Exactly How HRP Affects Your Outcome

• Get Your National Insurance Record (1978–today): Online, Phone & Post

• National Insurance Explained: Contributions, Credits, HRP (1978–2010)

Official GOV.UK links used in this draft

• Information to help answer common questions

• Quick guide to these resources – what they are and how to use them

• Home Responsibilities Protection: What you’ll get

• Home Responsibilities Protection: Eligibility