If you are widowed, a widower, or a surviving civil partner, it is natural to ask a very practical question: if Home Responsibilities Protection (HRP) was missed, could that increase what you receive now?

The careful answer is: sometimes, yes — but not in the simple way many families assume. HRP is not itself a separate sum that a surviving spouse or civil partner ‘inherits’. Instead, correcting missing HRP can change the National Insurance record or State Pension position that sits underneath a widow’s, widower’s or surviving civil partner’s entitlement.

That means there are usually three different questions to separate out. First: was the survivor’s own State Pension too low because their own HRP was missing? Second: was the deceased person’s State Pension too low because their HRP was missing? Third: does the widow, widower or surviving civil partner have an inheritance entitlement from the other person’s State Pension record under the old or new State Pension rules?

The short version

Missing HRP can matter after bereavement, but it does not automatically create a bigger survivor pension. In broad terms:

• if the survivor’s own HRP was missing, correcting it may increase their own State Pension or confirm that it stays the same;

• if the deceased person’s record was wrong, that may matter for underpayment checks or for what should have been inherited;

• the survivor rules depend heavily on whether the survivor and deceased reached State Pension age before or after 6 April 2016;

• some inheritance rights are lost if the survivor remarried or formed a new civil partnership before reaching State Pension age;

• in widow and widower cases, you are usually looking at a combination of HRP correction rules and separate inherited-State-Pension rules.

Start with the right question: whose record are you actually fixing?

This is the most common source of confusion. Families often say, “Mum was widowed — can she inherit because HRP was missing?” But before you can answer that properly, you need to identify whose record the missing years belong to.

Sometimes the missing HRP belongs to the widow herself because she claimed Child Benefit years ago and her National Insurance record never linked correctly. In that case, the core issue is her own State Pension entitlement. In other cases, the late husband, wife or civil partner may have had a pension history that affected what the survivor should have inherited. Those are not the same problem and they are not checked in the same way.

So the best opening rule is this: separate the survivor’s own HRP position from the survivor’s possible inheritance rights. Then look at how the two interact.

What GOV.UK says about inherited State Pension after a partner dies

The official GOV.UK bereavement and State Pension pages make two key points. First, extra State Pension based on a husband’s, wife’s or civil partner’s record depends on whether you reached State Pension age before or after 6 April 2016. Second, the amount you can receive is not a flat widow’s amount — it depends on the particular type of pension rights in issue and the dates involved.

If you reached State Pension age before 6 April 2016, you may be able to increase your basic State Pension through your spouse or civil partner’s National Insurance contributions and you may also be able to inherit some of their State Pension when they die. If you reached State Pension age on or after 6 April 2016, the new State Pension is mainly based on your own record, but you may still be able to inherit an extra payment on top in some cases.

That is why widow and widower HRP cases are often technical. The family may be looking at an old/basic State Pension issue, a new State Pension issue, an additional-State-Pension issue, a deferred-pension issue, or more than one of those at once.

How HRP fits into the widowed or surviving-partner picture

HRP originally protected parents and carers by reducing the number of qualifying years needed for the full basic State Pension, and later by converting into National Insurance credits where needed. GOV.UK also notes that, before 6 April 2016, some people who qualified for HRP because they got Child Benefit for a child under 6 or cared for someone on certain benefits may also have been entitled to Additional State Pension.

That matters because if HRP was missed, the knock-on effect is not always limited to the claimant’s own weekly pension. In some cases it may change the underlying pension position that later feeds into what a surviving spouse or civil partner should have received, or what an executor should ask DWP to review if the survivor has already died.

But the honest rule is still this: missing HRP does not automatically mean a widow, widower or surviving civil partner gets more money. GOV.UK’s official HRP support material says a successful claim can make State Pension increase or stay the same — it will not decrease. So even before you add the widow or widower inheritance rules on top, you should not assume there is always an arrears cheque waiting at the end.

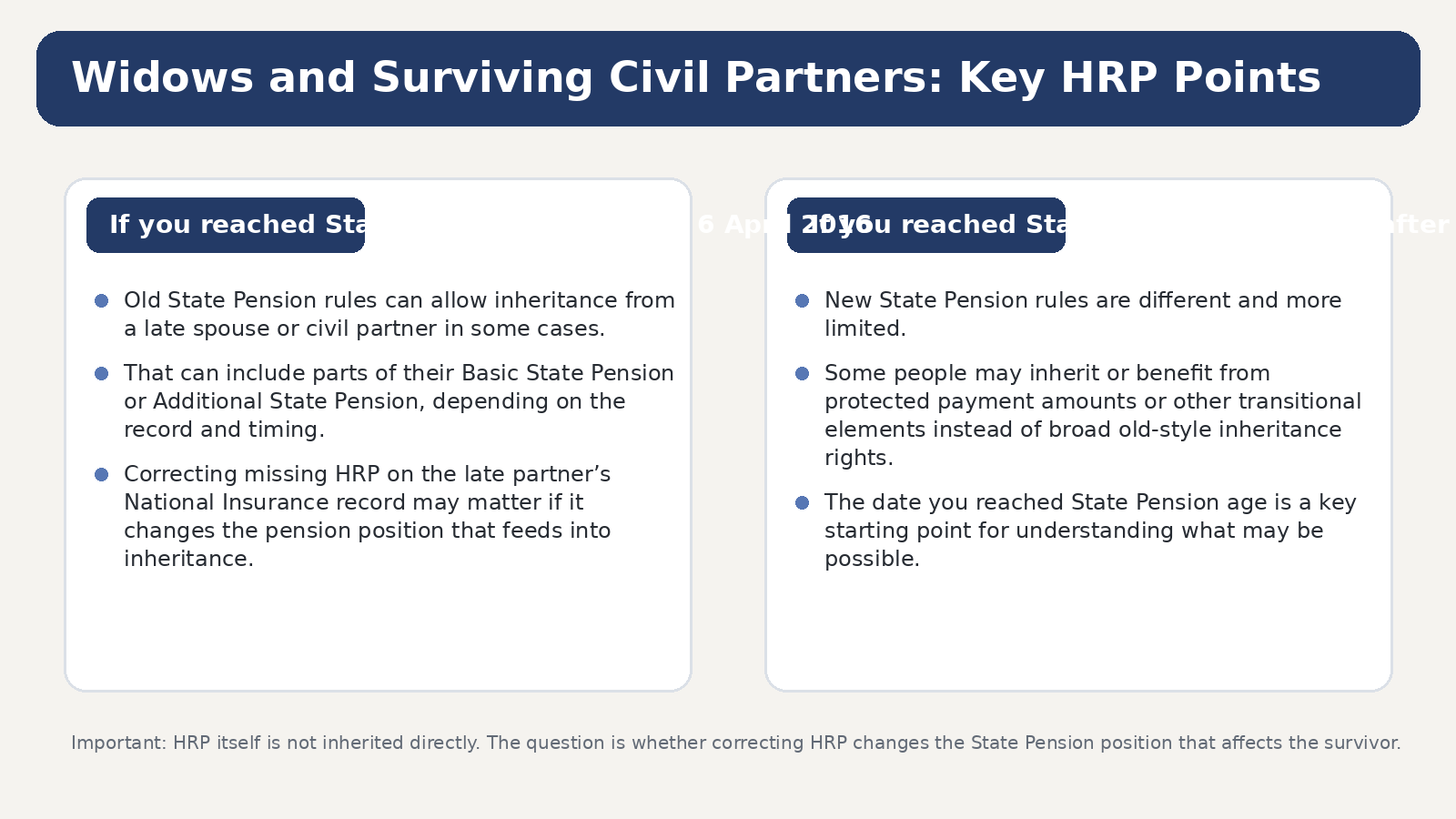

If the surviving partner reached State Pension age before 6 April 2016

This is the area where traditional widow and widower inheritance questions most often arise. GOV.UK says that if you reached State Pension age before 6 April 2016, you may be able to inherit some of your spouse’s or civil partner’s State Pension when they die. You may also be able to increase your own basic State Pension through their qualifying years if you do not already get the full amount.

In practice, that means a family should check at least four things:

• whether the survivor’s own National Insurance record was already complete or whether missing HRP may have reduced their own pension;

• whether the deceased spouse or civil partner had pension rights that the survivor should have inherited;

• whether the deceased had deferred State Pension or built up extra State Pension that can still pass across;

• whether remarriage or a new civil partnership before State Pension age blocks the inheritance route.

This is also the area where adult children sometimes discover that a widowed mother was underpaid for years, not because of one single error, but because more than one rule was missed at the same time.

If the surviving partner reached State Pension age on or after 6 April 2016

Under the new State Pension rules, the starting point is different. GOV.UK says the new State Pension is based on your own National Insurance record. However, a widow, widower or surviving civil partner may still be able to inherit an extra payment on top of their pension in certain cases, especially where the marriage or civil partnership began before 6 April 2016 and the deceased partner had rights that can still feed through.

This is one reason why HRP can still be relevant even in apparently “new State Pension” cases. If the survivor’s own record is wrong because HRP was missed, that may affect their own pension foundation. Separately, if the deceased partner’s pension history included elements that can still be inherited, the family may need to check that DWP has correctly reflected those too.

So the modern version of the question is not “Can I inherit HRP?” It is closer to: “After correcting missing HRP and checking the spouse’s or civil partner’s pension history, is there any extra amount I should now be receiving?”

When the issue is no longer about the living survivor but about the estate

There is another important scenario. Sometimes the widow, widower or surviving civil partner has already died. In that case, the next of kin or executor may still need to ask whether that person was underpaid because they did not inherit State Pension they were entitled to from a spouse or civil partner, or because HRP was missing and their own pension was too low.

DWP’s current deceased-underpayment guidance expressly says a person who has died may have been underpaid if they were widowed and did not inherit some of their husband’s, wife’s or civil partner’s State Pension. That is why some families have to look at two generations of pension history: the earlier spouse relationship, and then the estate position after the survivor’s death.

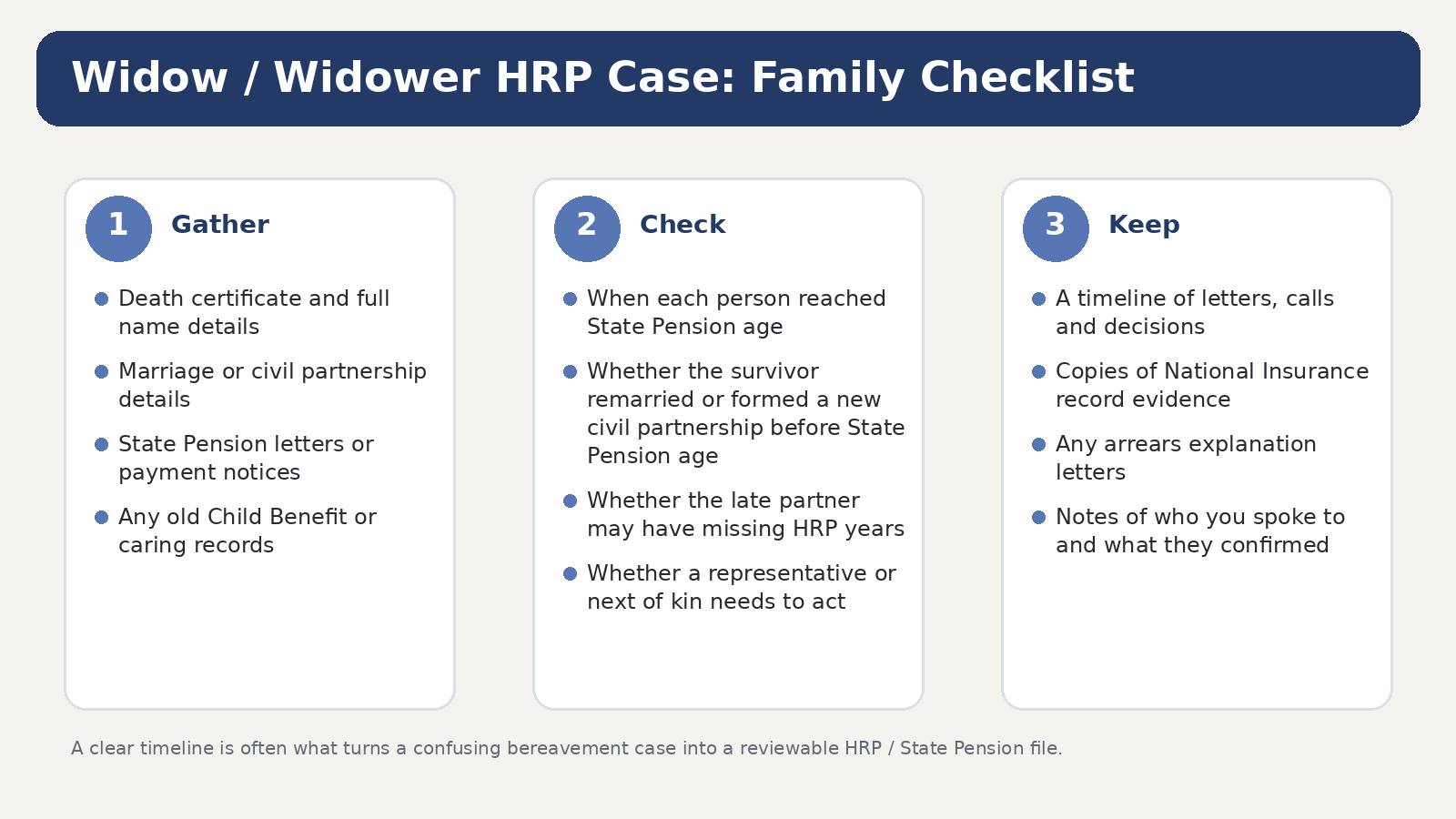

What documents and dates should families gather first?

Before contacting anyone, gather the documents that answer the core timeline questions. In most widow or widower HRP cases, the most useful starting bundle is:

• full names, dates of birth and National Insurance numbers if available for both partners;

• dates of marriage or civil partnership, and if relevant dates of separation, divorce, dissolution or remarriage;

• date of death of the spouse or civil partner;

• the survivor’s current State Pension letters or forecasts;

• any letters about Child Benefit, HRP, National Insurance gaps or historic pension decisions;

• notes showing who is acting now — the survivor, next of kin, executor or another authorised helper.

This saves a great deal of time because widow and widower cases usually turn on dates. The wrong assumption about one date can send you into the wrong rule set entirely.

Common mistakes families make in widowed HRP cases

The most common avoidable mistakes are:

• assuming HRP itself is inherited like a standalone asset;

• looking only at the deceased person’s record and ignoring the survivor’s own missing HRP years;

• assuming a successful HRP correction must always produce more money;

• forgetting that old/basic State Pension rules and new State Pension rules are different;

• ignoring remarriage or new civil partnership rules;

• failing to ask whether the estate should now request a deceased-underpayment review if the survivor has already died.

Check eligibility in 60 seconds

Final takeaway

Yes — missing HRP can matter in widow, widower and surviving-civil-partner cases. But the route is usually indirect. You are not “inheriting HRP” as such. You are checking whether missing HRP changed a pension position that affects either the survivor’s own State Pension, an inherited amount from a spouse or civil partner, or an underpayment that should now be reviewed.

That is why the safest approach is to work in order: identify whose record is wrong, identify which State Pension system applies, then ask the right office to review the right issue. Once families separate those steps clearly, these cases become much easier to understand.

Helpful internal Evanshaw blog links

• HRP for Deceased Relatives: A Practical Executor Guide (and why record retention matters)

• Posthumous HRP Claims — A Guide for Executors and Next of Kin

• Old vs New State Pension Rules: Exactly How HRP Affects Your Outcome (Tables & Worked Examples)

• HRP Support Pack: Official Common Questions Explained for Families

Official GOV.UK links used in this draft

• Home Responsibilities Protection: What you’ll get

• Information to help answer common questions

• Increasing or inheriting State Pension from your spouse or civil partner

• Inheriting or increasing State Pension from a spouse or civil partner (new State Pension)

• Your benefits, tax and pension after the death of a partner — pensions

• Request information about underpaid State Pension for someone who has died