If you have discovered that your mum or dad may be missing Home Responsibilities Protection (HRP), one of the first worries is often practical rather than technical: who is actually allowed to help?

That is a sensible question. Families often want to do the right thing, but they do not want to overstep. In many cases, a parent can still understand the issue, decide what they want to do, and sign what needs signing. In that situation, you may not need a Lasting Power of Attorney (LPA) just to help them read letters, gather evidence, sit with them on a call, or organise paperwork.

Where families go wrong is assuming one of two extremes: either ‘I cannot do anything unless I have LPA’, or ‘I am their son or daughter so I can take over the whole claim’. Neither is automatically right.

First, remember who does what in an HRP case

The HRP application itself sits with HMRC. GOV.UK says you can use the online service or postal form CF411 to apply for Home Responsibilities Protection. If a claim is successful for someone already receiving State Pension, the Department for Work and Pensions (or the Department for Communities in Northern Ireland) reviews the pension award.

That split matters because families sometimes think DWP can simply ‘fix HRP’. Usually the route starts with the HRP application and the National Insurance record, and only then feeds into the pension side.

• HMRC: HRP application, supporting evidence, National Insurance record correction.

• DWP / Pension Service: State Pension information, recalculation, arrears and related pension contact once the record is corrected.

• Your family’s role: work out who is allowed to speak, sign and manage the case at each stage.

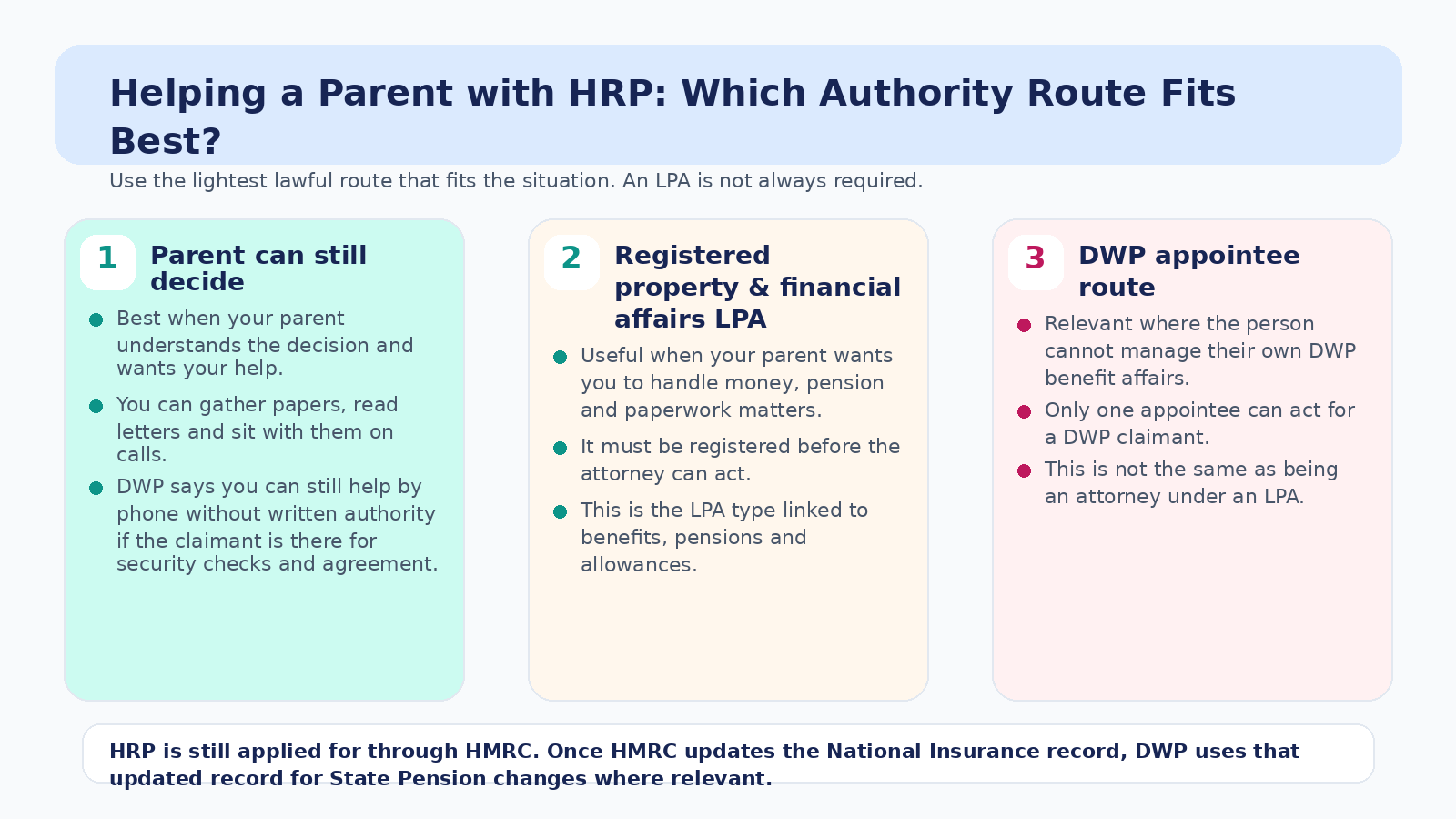

Do you always need an LPA to help a parent with HRP?

No. Not always.

If your parent can still understand the decision and wants your help, the safest starting point is often the simplest one: keep them at the centre of the process. They may still read the papers, decide what they want to do, and sign the forms themselves while you help with the practical legwork.

That means many families can do a lot without jumping straight to formal legal arrangements. You can help them read the GOV.UK guidance, find old Child Benefit evidence, organise a timeline, draft notes for a phone call, or sit with them while they make contact.

In plain English: helping is not the same as taking over.

When a Lasting Power of Attorney does become useful

An LPA becomes much more relevant where your parent wants you to manage financial and pension matters for them, or where dealing with letters, deadlines and official calls has become unrealistic.

The important point is the type of LPA. GOV.UK makes a clear distinction between:

• a property and financial affairs LPA; and

• a health and welfare LPA.

For HRP, National Insurance and State Pension matters, it is the property and financial affairs LPA that matters. The official LPA guide says this type can be used for things such as managing bank accounts, paying bills and dealing with benefits or pensions once it is registered.

That is why families should not assume that any LPA will do. A health and welfare LPA is about care, treatment and day-to-day welfare decisions, not routine financial administration.

LPA is not the same thing as being an appointee

This is a common point of confusion.

DWP says written authority can include an LPA, an EPA, deputyship or an appointee arrangement. But an appointee is a separate route. GOV.UK explains that an appointee is used where someone cannot manage their own benefits affairs.

So, if your parent still has capacity and simply wants help, an appointee route may be unnecessary. If they cannot manage their own DWP benefit affairs, an appointee arrangement may be the more relevant route.

The practical takeaway is simple:

• Parent has capacity and wants help: keep them involved; they may still sign and speak for themselves.

• Parent wants you to manage money and pension matters more formally: check for a registered property and financial affairs LPA.

• Parent cannot manage their own DWP benefit affairs: look at the appointee route for DWP benefits.

Do not use the words ‘attorney’ and ‘appointee’ as if they mean the same thing. They do not.

What evidence should families gather before sending an HRP application?

This is another area where families can make real progress, with or without formal authority.

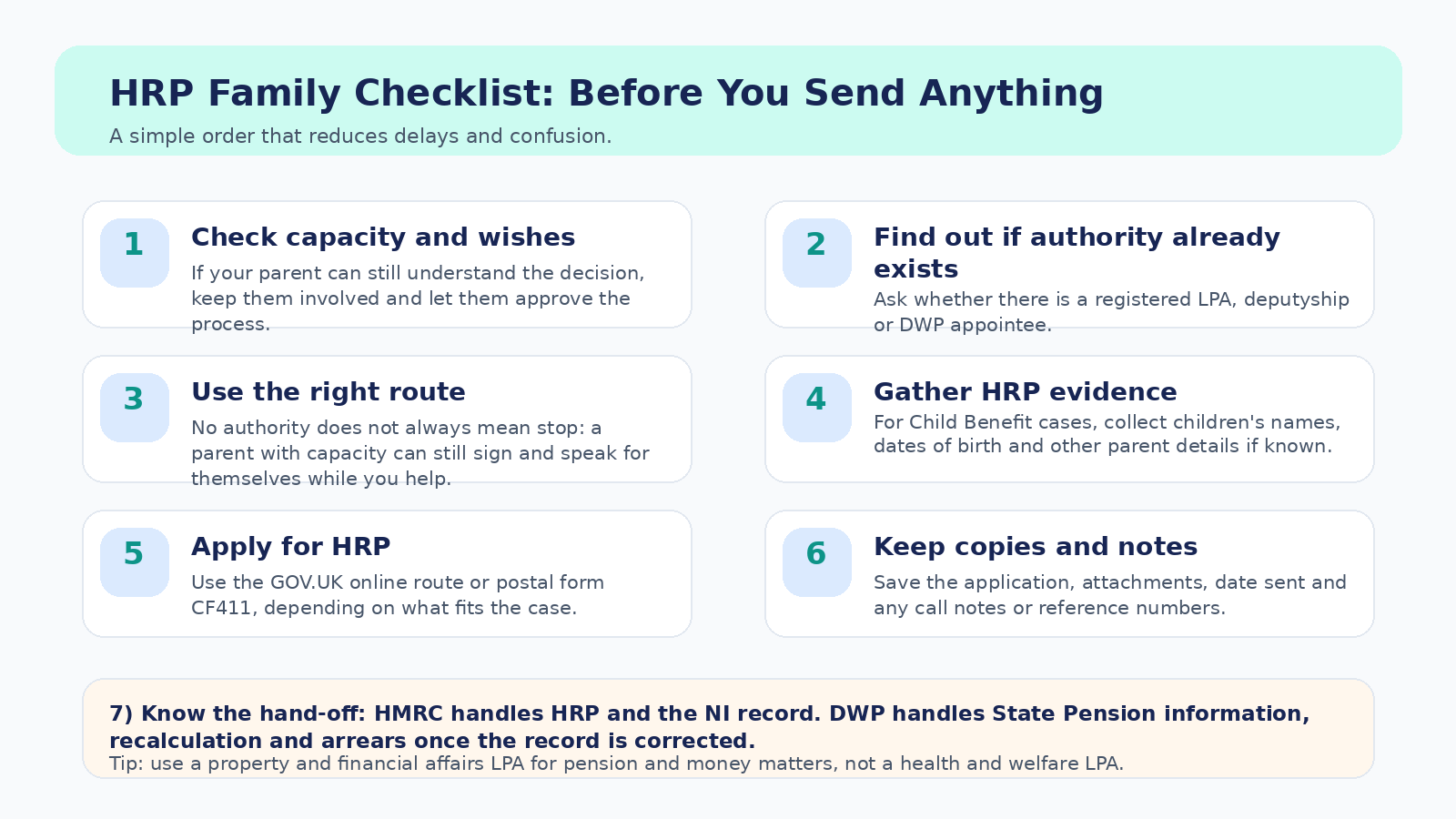

HMRC’s HRP guidance says that if the case is based on Child Benefit, you will need the names of all children, the dates of birth of all children, the date Child Benefit started, and details of who received it. If the claim is based on caring, the evidence depends on the caring route involved.

Before you send anything, create one clean pack:

• a short timeline of the years you think HRP should cover;

• children’s names and dates of birth;

• other parent details if known;

• copies of any benefit letters, old correspondence or supporting records;

• notes of name changes, address changes or anything that may explain record mismatches.

Even where a child or other relative is doing most of the organising, good file order matters. It reduces the chance of sending an incomplete or confusing pack.

A calm step-by-step plan for families

If you are helping a parent with HRP, work in this order:

• Check whether your parent can still understand the issue and make the decision themselves.

• Ask what help they want from you. Some parents want support, not substitution.

• Find out whether there is already a registered property and financial affairs LPA, deputyship or DWP appointee arrangement in place.

• Gather the HRP evidence before you start sending forms.

• Use the official HMRC route for the HRP application.

• Keep copies of everything sent, plus dates, reference numbers and call notes.

• If your parent is already State Pension age, remember the pension side usually follows after the NI record is corrected.

Mistakes families make again and again

The most common avoidable mistakes are:

• assuming that being a close relative automatically gives you authority to manage the whole case;

• assuming that a health and welfare LPA covers pension and money paperwork;

• taking over too early when your parent can still decide and sign for themselves;

• confusing the HRP application stage with the later State Pension recalculation stage;

• sending disorganised evidence and then struggling to prove what was sent.

Check eligibility in 60 seconds

Final takeaway

The best family support is usually calm, organised and proportionate. Start with your parent’s wishes and capacity. Use the lightest lawful route that fits the situation. If they can still decide and sign, help them without taking over. If they need formal support with financial and pension matters, a registered property and financial affairs LPA may become important. If they cannot manage their own DWP benefit affairs, the appointee route may be the better fit.

That approach is usually better for the parent, cleaner for the paperwork and easier for HMRC or DWP to follow.

Helpful internal Evanshaw blog links

• HRP Support Pack: Official Common Questions Explained for Families

• How to Claim HRP (CF411) — Simple 5-Step Guide (Online or Post, incl. Partner Transfer)

• What Is My National Insurance Record (NPS) — and How Do I Get It?

• What Is a DWP State Pension Forecast (and How to Read It for HRP)?

• How Long Do HRP Claims Take? Timeline, Tracking, and What to Do If You Hear Nothing

Official GOV.UK links used in this draft

• Apply for Home Responsibilities Protection

• Manage someone’s claim for them

• Make, register or end a lasting power of attorney

• Lasting power of attorney: acting as an attorney — property and financial affairs