If you receive a successful Home Responsibilities Protection (HRP) decision and then a State Pension arrears payment, one of the first questions people ask is simple: “Will I have to pay tax on this?”

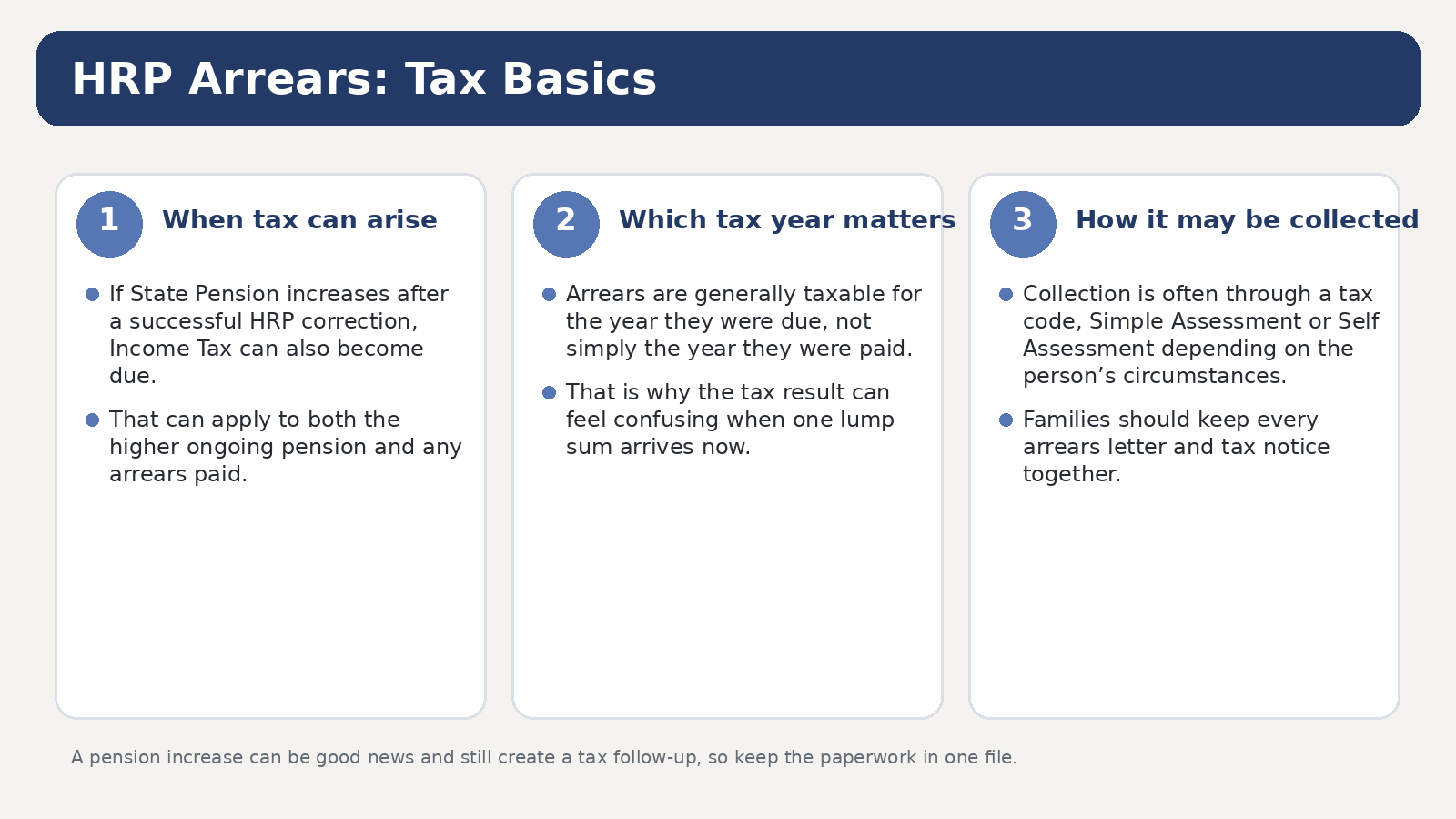

The official answer is yes, potentially — but the tax rules are more specific than many families expect. GOV.UK’s current HRP guidance says that if missing HRP is added successfully, your State Pension may increase or stay the same, and you may also receive arrears. It also says that HMRC will collect any Income Tax due on both the increase in State Pension and on any arrears paid.

The second important question is whether the wider knock-on effects stop with tax. They do not always. GOV.UK also says that if your State Pension increases, it could affect the amount of benefits you are entitled to, including Pension Credit. So this is not just a “tax bill” topic. It is really about what changes after a successful correction, who needs to be told, and what paperwork you should keep.

The short version

• HRP arrears can be taxable, and HMRC says tax may also be due if your ongoing State Pension rises;

• payments of State Pension arrears are taxed as income for the year they were due, not the year they were actually paid;

• HMRC says any tax due is normally collected through your tax code where possible;

• if you already file a Self Assessment return, you must report the arrears there;

• if you do not usually file tax returns, you may instead receive a Simple Assessment bill from HMRC;

• a higher State Pension can also affect Pension Credit and possibly other income-related benefits, so changes should be reported promptly.

What GOV.UK actually says about tax on HRP arrears

The clearest official source for this topic is GOV.UK’s HRP common-questions guidance. It says that if your claim is successful, your State Pension will increase, or stay the same — it will not decrease. It also says you may be entitled to arrears and that HMRC will collect any Income Tax due on an increase in State Pension and on any arrears paid.

That same guidance contains the point many people miss: payments of State Pension arrears are taxable as income for the year they were due, not the year they are paid. So if a lump sum lands in your bank account now, the tax treatment does not simply work as though it all belongs to the current tax year.

GOV.UK also says HMRC limits collection of the tax due to the current year and the 4 previous years. For many claimants, that is a reassuring detail because it means a successful HRP correction does not automatically open up unlimited historic tax collection.

Does that mean everyone will owe tax?

No. Whether you owe any tax depends on your overall taxable income. GOV.UK says if your total taxable income exceeds your Personal Allowance, you will be subject to Income Tax at the appropriate rate. If the increase pushes part of your income into a higher tax band, only the portion that falls within that higher band is taxed at the higher rate.

In plain English, that means an arrears payment can be taxable without creating a dramatic tax outcome for everyone. Some people will still remain below the relevant threshold. Others may owe some tax, but only on part of the extra income. The figure depends on the years the arrears relate to and the person’s total taxable income position.

How HMRC usually collects the tax

GOV.UK says any tax due will be collected through your tax code where possible. If the person already files a Self Assessment return, the arrears must be reported on that tax return. If they do not normally complete tax returns, they may instead receive a Simple Assessment bill from HMRC.

That is why families should not ignore a later HMRC letter just because the HRP claim itself was successful. The pension correction and the tax follow-up are two different parts of the story.

What about Pension Credit and other benefits?

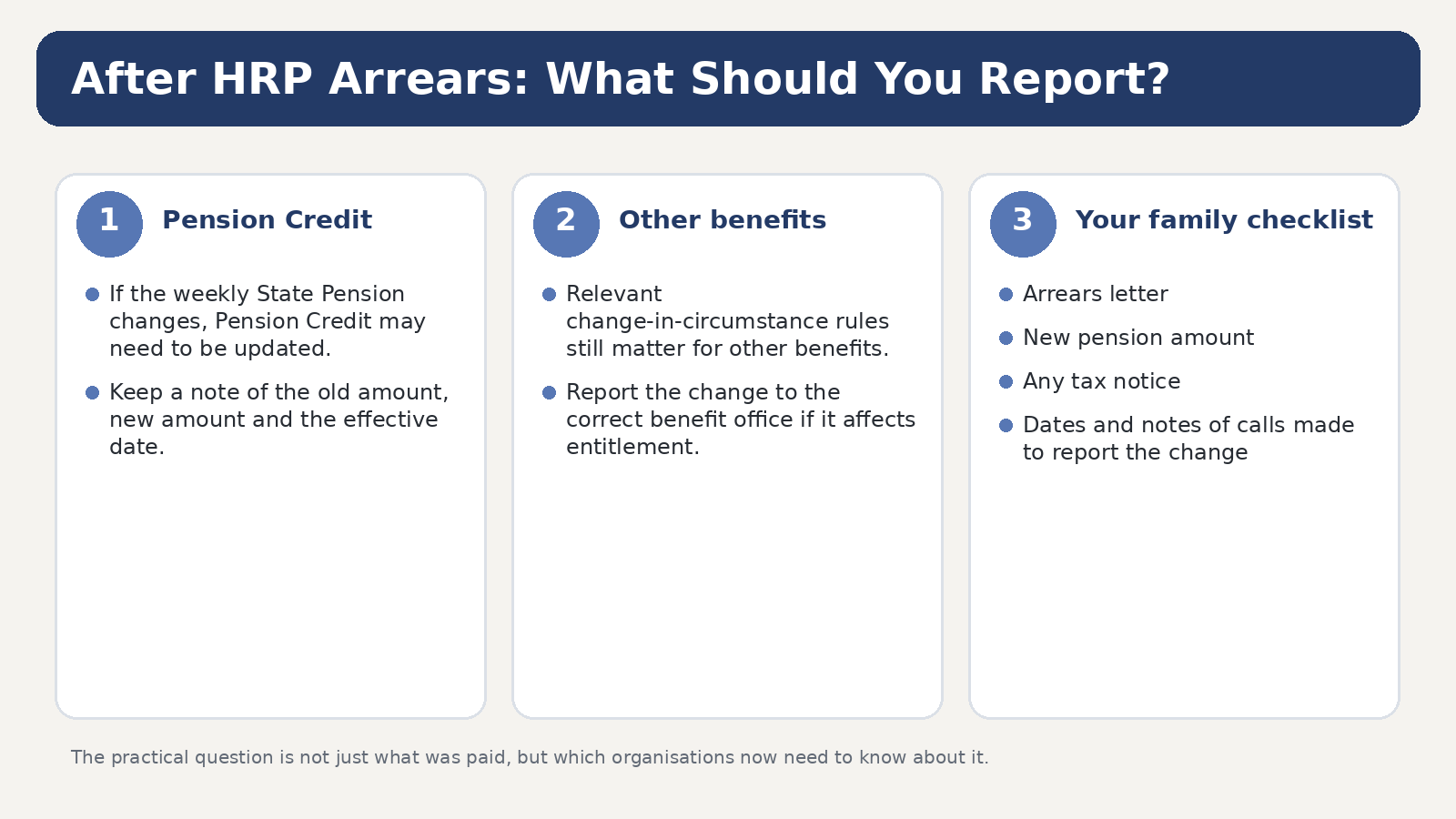

This is where Blog 8 deliberately goes wider than a simple tax explainer. GOV.UK’s HRP guidance says that if your State Pension increases, it could affect the benefits you are entitled to, including Pension Credit. In other words, a successful HRP outcome can change more than the weekly pension itself.

GOV.UK’s Pension Credit guidance separately says you must report changes to personal and financial circumstances, and it warns that a claim might be stopped or reduced if changes are not reported straight away. So if the corrected HRP result changes the ongoing State Pension figure, families should assume the updated pension amount needs to be reported.

If you receive Housing Benefit or other benefits that depend on income, GOV.UK’s general benefits change-of-circumstances guidance also points claimants to report relevant changes. The safest practical habit is simple: once the revised State Pension figure is confirmed, update each benefit office that needs the new number rather than assuming the systems will all align automatically.

The point many people get wrong about arrears

A common misunderstanding is to focus only on the lump sum. The more important long-term issue is often the revised weekly pension. A one-off arrears payment may matter for tax, but the ongoing weekly amount is what most directly feeds into Pension Credit and other income-related assessments.

So when you receive a successful HRP outcome, do not stop at the arrears figure. Check all three things separately:

• the corrected National Insurance record;

• the revised weekly State Pension amount and the date it takes effect;

• any separate HMRC tax follow-up or benefits adjustment.

What paperwork should you keep?

For this type of case, good record-keeping matters more than families expect. Keep the HRP decision, the revised State Pension letter, any arrears explanation, and any later HMRC tax letter together in one file. If you notify Pension Credit or another benefit office, keep a note of the date, the updated figure you gave them, and who you spoke to.

This matters because months later the family may remember the arrears but forget the effective date of the weekly increase, or remember the new weekly amount but lose the HMRC follow-up. Those details are exactly what later reviews depend on.

Common mistakes to avoid

• assuming arrears are always tax-free because they relate to an old error;

• thinking the whole lump sum is automatically taxed as income of the year it was paid;

• ignoring a later Simple Assessment or Self Assessment reporting requirement;

• focusing on the arrears but forgetting to report the revised weekly pension to Pension Credit;

• assuming a successful HRP decision cannot affect other means-tested benefits.

Check eligibility in 60 seconds

Final takeaway

Yes — HRP arrears can be taxable, and yes — a successful HRP correction can also affect Pension Credit and other benefits. But the right response is not panic. It is orderly follow-up.

The safe sequence is: keep the HRP decision, check the revised weekly pension, watch for the HMRC tax position, and report the change wherever your benefits depend on income. Once you break it into those steps, this becomes far easier to manage.

Helpful internal Evanshaw blog links

• HRP and Pension Credit — What Changes When Your State Pension Goes Up?

• How Much Is a Successful HRP Claim Worth? (Back Pay, Pension Uplift & Examples)

• What Is a DWP State Pension Forecast (and How to Read It for HRP)?

• Old vs New State Pension Rules: Exactly How HRP Affects Your Outcome (Tables & Worked Examples)

• HRP Support Pack: Official Common Questions Explained for Families

Official GOV.UK links used in this draft

• Information to help answer common questions

• Pension Credit: report a change of circumstances

• Benefits: report a change in your circumstances