Getting a successful Home Responsibilities Protection (HRP) decision can feel like the finish line. In reality, it is often the handover point between the National Insurance record stage and the pension stage.

That is why families are often left asking the same question: ‘HMRC has accepted it — so what actually happens now?’ The answer depends mainly on whether the person is already over State Pension age and whether the corrected years change the final pension calculation.

Official GOV.UK research says that once an HRP application is processed, HMRC updates the customer’s National Insurance record and, if they are of State Pension age, shares that information with DWP so any State Pension change and arrears due can be processed.

The short version

If HMRC accepts missing HRP, the order is usually this:

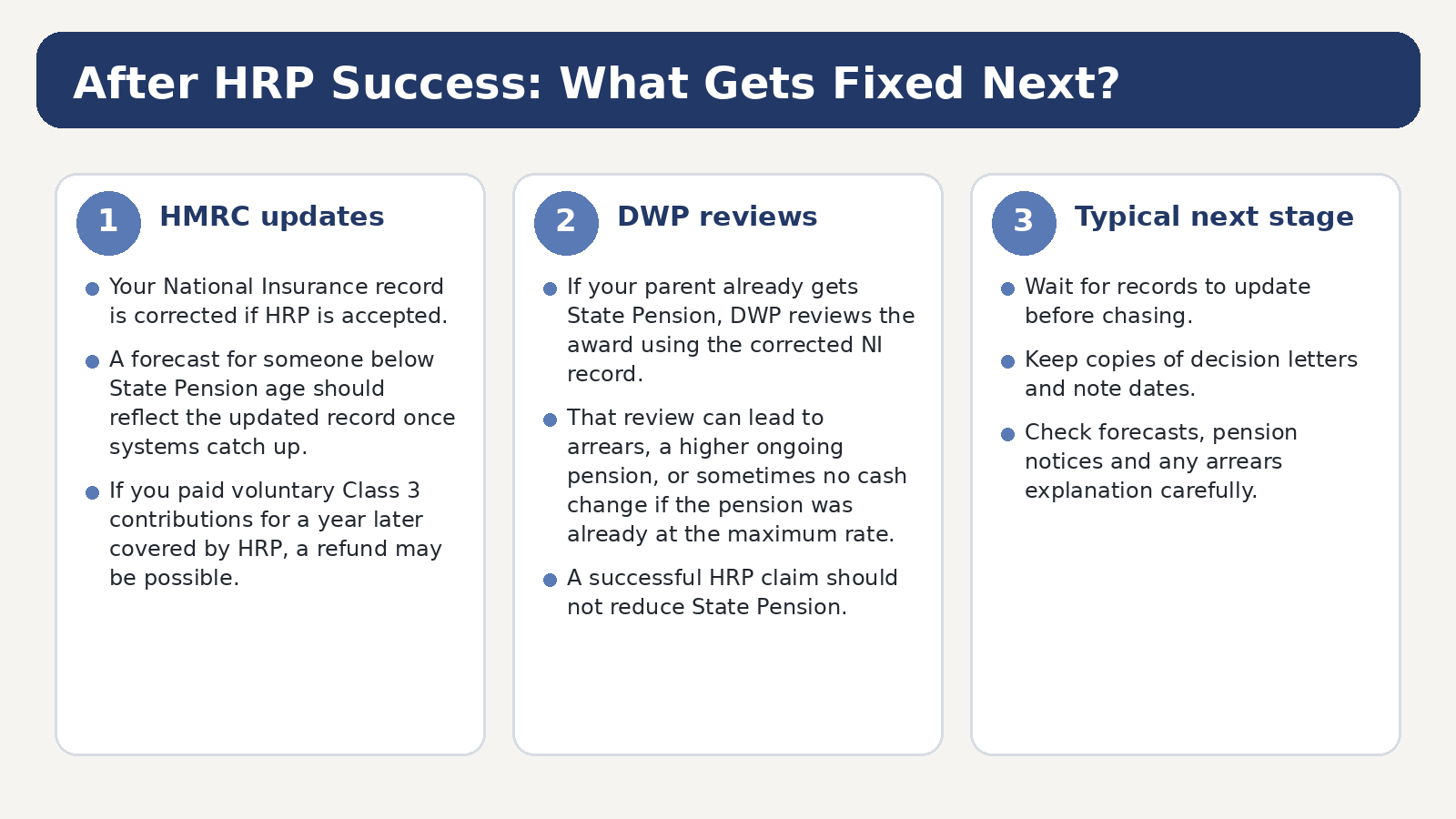

• HMRC corrects the National Insurance record.

• If the person is already receiving State Pension, DWP (or the Department for Communities in Northern Ireland) reviews the pension award.

• If the person is not yet at State Pension age, the official change is usually to the National Insurance record and future State Pension forecast.

• If the successful HRP years change the pension outcome, there may be a higher ongoing pension and arrears due.

• If the corrected years do not change the final entitlement, the pension may stay the same. GOV.UK’s official HRP communications say a successful claim can increase the State Pension or leave it unchanged — it will not reduce it.

Step 1: HMRC updates the record first

The first thing to remember is that HRP sits on the National Insurance side of the system. So even after a successful outcome, the first concrete change is usually to the National Insurance record itself.

This matters because many people expect an immediate pension letter or payment. In practice, the record-correction stage comes first. That updated record is then what feeds the pension calculation side.

If you are checking progress, it often helps to think in two layers: record corrected first, pension result second.

Step 2: What happens if the person is already getting State Pension

GOV.UK’s current HRP support guidance is clear on this point: if the person is already receiving State Pension, DWP or the Department for Communities in Northern Ireland will review the pension award. The same official guidance says you do not need to contact them just because HRP has been accepted.

That is useful because it stops families chasing the wrong office too early. The pension review is supposed to follow from the corrected record.

In plain English, the case usually moves from ‘Was HRP missing?’ to ‘Does this corrected record change the amount that should have been paid?’

Step 3: What happens if the person is not yet at State Pension age

The official HRP communications give a different answer for people who have not reached State Pension age yet: if the claim is successful, the State Pension forecast will be updated.

That means the value of a successful HRP correction is still real, even without an immediate cash payment. The corrected years can improve the future pension position and may reduce the need to think about voluntary National Insurance top-ups for the same years.

So, for someone below State Pension age, the practical next checks are usually: Has the National Insurance record changed? Has the forecast changed? Does the forecast still suggest paying Class 3, or has that question become smaller?

Will a successful HRP decision always produce arrears?

No. Not always.

This is one of the most important points to explain carefully. A successful HRP correction does not automatically mean a lump sum is due. GOV.UK’s own HRP communications say a successful claim can increase the pension or leave it unchanged. DWP’s HRP underpayment progress release also explains that not all processed cases produce an underpayment because some people may already have a full State Pension, may already receive a higher inherited pension, or may still not become entitled after the record is reviewed.

So the better expectation is this: acceptance is a strong positive result, but the money outcome still depends on what the corrected years do to the final pension calculation.

Step 4: What might actually change after approval

Depending on the case, the post-acceptance result may be one or more of the following:

• a higher weekly State Pension going forward;

• arrears for past underpayment periods;

• an updated forecast if the person is below State Pension age;

• no cash change, if the corrected HRP does not alter the final entitlement.

This is also where the older/basic State Pension rules and the newer State Pension rules can matter. HRP affected those systems differently, which is why some accepted cases have a bigger uplift than others.

Step 5: Do not ignore tax and means-tested benefits

GOV.UK’s official HRP common-questions page says that if the State Pension increases, it could affect the amount of tax you pay or the benefits you are entitled to, including Pension Credit. The same page says HMRC will collect any Income Tax due on an increase in State Pension and on any arrears paid.

That does not mean a successful outcome is a bad one. It simply means the household should look at the bigger picture after the pension result lands, especially where Pension Credit, Council Tax support or other income-related help may be involved.

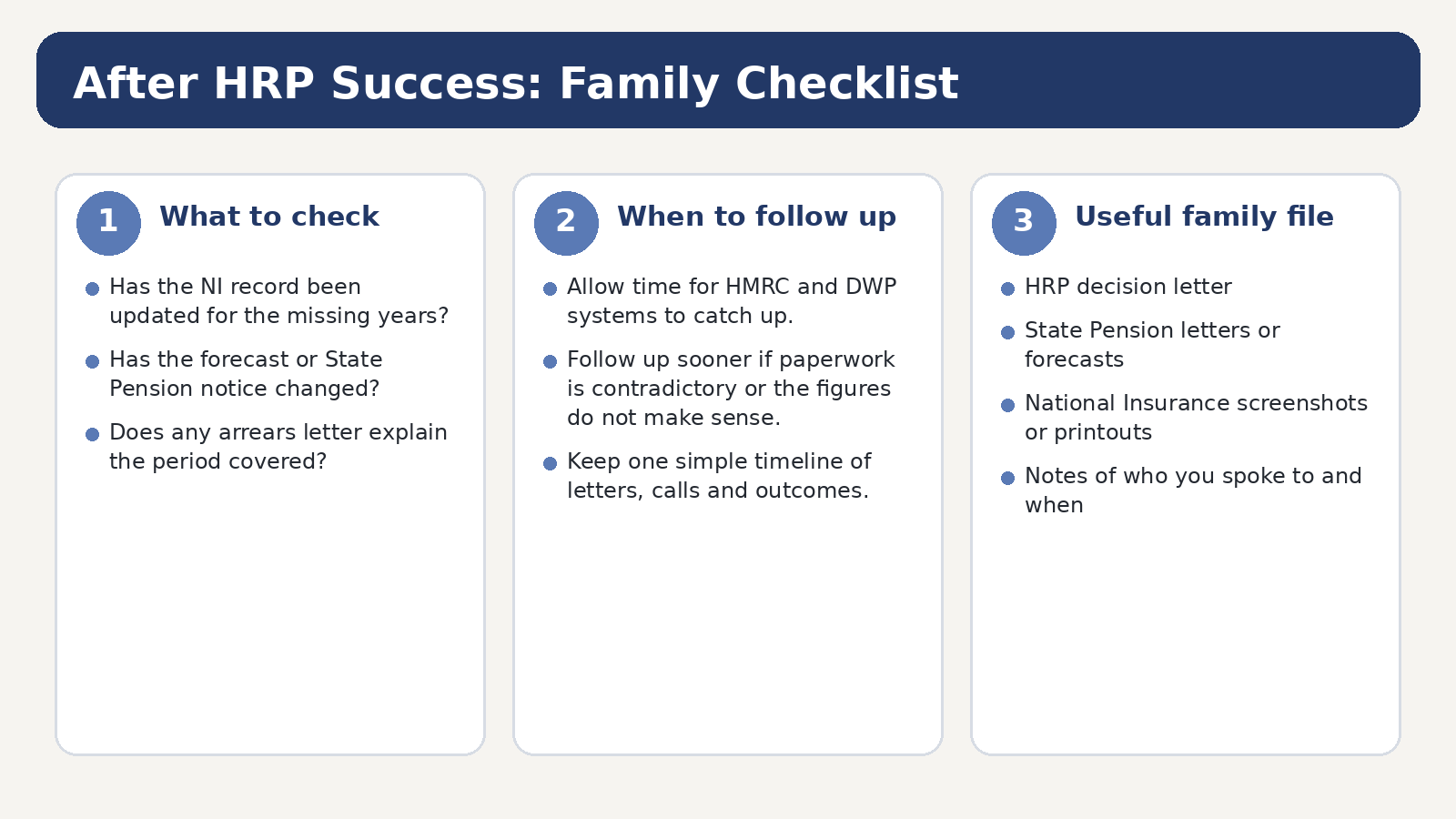

What should you keep after HMRC accepts HRP?

Once a case has moved into the pension stage, good record-keeping becomes even more useful. Keep:

• a copy of the successful HRP correspondence or online confirmation;

• the updated National Insurance record if you can access it;

• any new State Pension forecast or pension award letter;

• notes of dates, reference numbers and phone calls;

• bank-entry dates for any arrears paid.

That paper trail makes it much easier to spot whether the case has fully completed or whether a follow-up is still needed.

Common mistakes after a successful HRP outcome

The most common avoidable mistakes are:

• assuming acceptance always means a lump-sum arrears payment;

• contacting the wrong department before the record has had time to feed through;

• failing to compare the ‘before’ and ‘after’ pension position;

• ignoring possible knock-on effects for tax or Pension Credit;

• throwing away key letters once the first good news arrives.

Check eligibility in 60 seconds

Final takeaway

A successful HRP decision is important — but it is not always the end of the story. First the National Insurance record is corrected. Then, if relevant, the pension side catches up. Some people see a higher pension and arrears. Others see no cash change because the corrected years do not alter the final entitlement. What should never happen, according to GOV.UK’s HRP communications, is a successful claim reducing the pension.

If families understand that sequence, they are much less likely to panic during the gap between ‘accepted’ and ‘fully reflected in the pension’. That gap is usually where the confusion lives.

Helpful internal Evanshaw blog links

• Old vs New State Pension Rules: Exactly How HRP Affects Your Outcome (Tables & Worked Examples)

• How Long Do HRP Claims Take? Timeline, Tracking, and What to Do If You Hear Nothing

• HRP and Pension Credit — What Changes When Your State Pension Goes Up?

• What Is a DWP State Pension Forecast (and How to Read It for HRP)?

Official GOV.UK links used in this draft

• Apply for Home Responsibilities Protection

• Quick guide to these resources – what they are and how to use them

• Information to help answer common questions

• Exploring take-up of missing Home Responsibilities Protection

• HRP State Pension underpayments: progress on cases reviewed to 30 September 2024